Once businesses get big, they want to keep it that way

Despite a raft of new regulations designed to make markets more competitive, Big Tech & Big Payments still wield a lot of control and pricing power, but could this be about to change?

“No field sees winners try to retract the ladder behind them more aggressively than business”, says Scott Galloway, and he’s right.

Anti-competitive behaviour is everywhere; Apple's App Store levies a 30% tax on all developers; Google search advertising sits on both sides of the negotiating table and owns the damn table; Amazon's marketplace favours its own products and prohibits partner sellers from offering lower prices elsewhere, all while copying bestsellers and turning them into Amazon-branded goods; Microsoft abuses distribution advantages across its Office suite, and until recently Meta had a near monopoly on social media advertising.

Let's not forget that these trillion-dollar companies were once scrappy startups that disrupted incumbents and created new categories.

But it's a simple fact of capitalism that once you get big and have market power, you try to keep it that way.

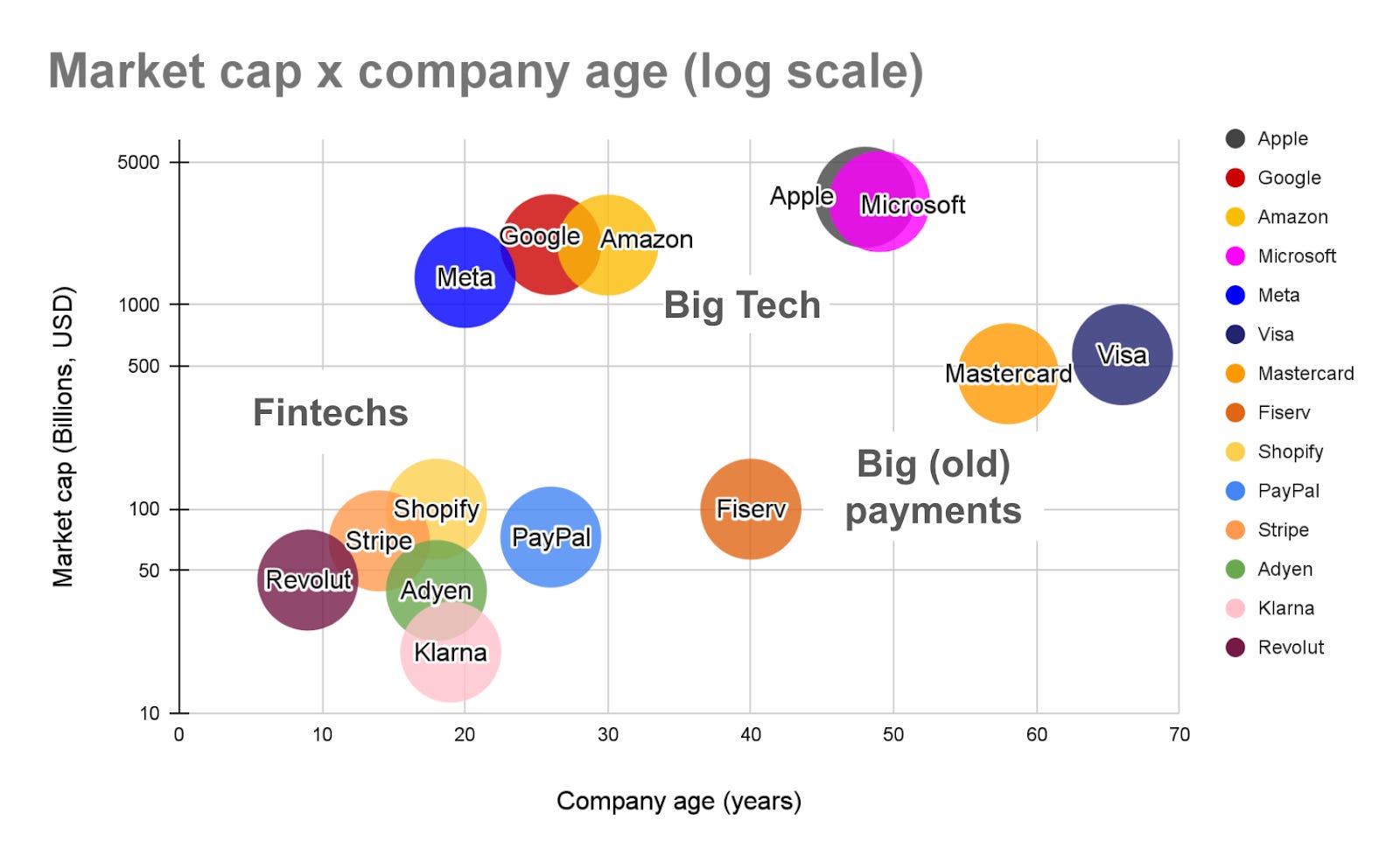

The payments duopoly

In payments, Visa and Mastercard are an indomitable duopoly that have again dodged a major fine from regulators.

Earlier this year, the presiding judge threw out a $30 billion DOJ settlement to compensate merchants for inflated interchange fees that resulted from alleged collusion between schemes and issuers. (More details on why are in my footnote.)

And last week, the American Department of Justice sued Visa, accusing it of:

“pressuring merchants and partners to go along with debit card practices that stifle the payment giant’s rivals”.

These captive pricing tactics aren’t as egregious as the €5 bottles of water you have to buy at the airport to avoid dying of dehydration – but they have a lot in common.

Prodigies who lost their way

In payments, Visa and Mastercard are given so much attention because they are bigger, more ubiquitous, older, and more treacherous than the rest.

And age matters when it comes to exerting influence over younger rivals.

But so does mindset. As the great Italian cyclist, Fausto Coppi famously said:

“Age and treachery will overcome youth and skill”

There is one fintech that was once a child prodigy. But like many child prodigies (Macaulay Culkin, Jennifer Capriati, Haley Joel Osment, Britney Spears), it lost its way and is still battling an addiction to incremental product improvements.

PayPal has become a comparative minnow because of the historically unprecedented growth of Big Tech and “the duopoly.” But it’s still a big beast in Europe, where it is comfortably within the top 50 companies by market cap, equivalent to Shopify or Munich Re.

By comparison, Google, founded in the same year (1998), is currently worth 27 PayPals. Visa is worth 7.8.

This is in large part due to PayPal’s languishing stock performance from mid-October 2020 to present, PayPal’s stock is down 66% since then, compared to Fiserv which is up 56%, Mastercard up 38% and Visa up 26%.

Down, but by no means out

Despite a relative decline, and all things are relative, PayPal still wields enormous power, especially in Germany, where it has a 28% share of online payments and 35 million active users (that's more than 50% of the adult population).

It has built and maintained a number of competitive moats—not just its trusted consumer wallet that offers payment protection—which makes it difficult to dislodge from a rigid, complex, and interconnected payments system. But it’s about to face a new onslaught from dissatisfied merchants and fintech offering, among other things, more affordable payment methods to merchants. So, without further ado…

What are the top three things PayPal merchants complain about?

Pricing power: PayPal knows that, depending on your vertical, between 25% and 75% of your customers use PayPal as their preferred online payment method at least once a month. So when it comes to negotiating fees, even for merchants with volumes that put them comfortably in the mid-market segment, there is no negotiation. Pay your payment tax of circa 2% + 0.35 cents per transaction, and shut up.

Withholding merchant funds over transaction disputes: PayPal's active users are its most valuable asset and merchants want them because they convert well when they see the little blue logo. PayPal know this. Which means favour the buyer in a transaction dispute, to the chagrin of merchants. Two DACH based e-commerce merchants I have spoken with had over €300,000 of their funds frozen for three months over a handful of €250 transaction disputes. What’s worse, these transactions were clearly fraudulent. This imbalance is threatening the viability of some businesses, and even for those with sufficient cash flow, it is still an unacceptable infringement on working capital.

Unresponsive merchant services : It's well known that PayPal's merchant support services are poor, and that more businesses than can be named have wasted hours listening to PayPal's hold music, which I can only presume is Mo Money, Mo Problems, swiftly followed by Money Worries; both of which are absolute tunes to be fair.

PayPal’s playbook is deliciously treacherous, calculating and well rehearsed. But for how much longer can it keep operating in this way?

Merchants will soon have more levers than ever before to tip the scales back in their favour. So, let’s look at four: the carrot, the stick, the strong nudge, and the breakup.

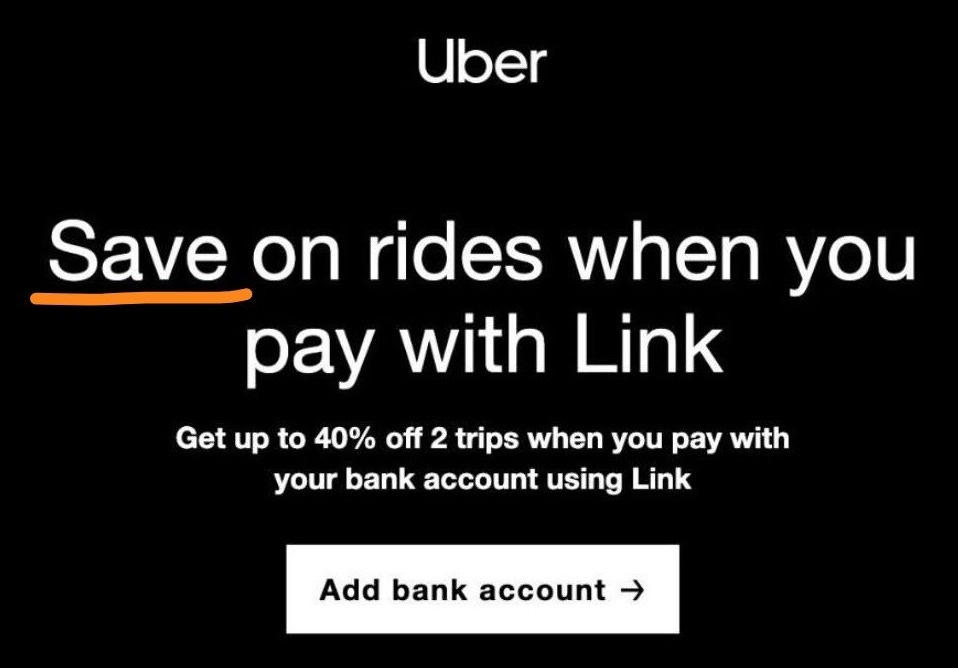

🥕 The carrot : discounting or incentives

Provide an incentive for customers to use a cheaper payment method that accelerates user adoption beyond what you could have achieved organically, a.k.a. shift processing volume away from PayPal.

Uber ran a promotion earlier this year offering 40% off two trips if customers paid from their bank account. The business case is based on the assumption that once a customer links Pay by Bank to their Uber wallet, they will continue to use it, and Uber will realise savings from lower transaction fees over multiple future trips. This mechanic makes a lot of sense for a higher frequency/repeat purchases type business like Uber. Variations of this tactic are to offer an enhanced benefit like cashback or free next-day delivery to attract first time users.

🏑 The stick : surcharging

Definition: Charging customers a fee for using a particular payment method. This is allowed in the US for certain card types, and new EU regulations should allow European merchants to levy a surcharge, but with a cap.

The problem is that this is not permitted by PayPal's T&Cs. But doing it will get the attention of an account manager and force a conversation about rates and terms. (This applies more to larger merchants; smaller ones are easier to ignore). The concern for merchants, however, is a drop in conversion rates if customers do not see a payment method they are willing or able to use to complete the purchase. Kudos to Lieferando for surcharging payment providers wanting to takeaway control. (Sorry, couldn’t help myself). I have also seen a Swiss ticketing platform surcharge for PayPal and spoken to a number of merchants in Germany and Austria who are considering doing so.

🫸🏼 The strong nudge

Give the customer a good reason to try something else, design the customer journey to remove as many barriers to conversion as possible (e.g., having to set up a user account or download an app), overcommunicate, and show trusted bank logos. Or, if you want to go the full hog, preselect said cheaper payment method and give it top presentation in the checkout.

It works.

💔 The breakup

Find a new partner, test them out, once they convert reliably, turn off PayPal for a while, maybe forever. Remember, you need space and you're at a point in your life where you should be saving money for the future, because life is long and business is tough.

Regulators, walk the line

Here is a controversial statement : A more affordable future for online merchants is being enabled by EU regulators.

As easy as it is to castigate doughy Brussels bureaucrats, payments regulations like PSD2 have helped a new generation of European fintechs climb into the ring and take a swing at two 800-pound gorillas. (And give PayPal, standing off to one side with an XL tub of Vaseline and a towel, a look that says "rest one eye up").

Remember, change in payments takes time. To paraphrase Dr Michael Salmony, who spoke at this year's Merchant Payments Ecosystem (MPE):

"Nothing significant in payments happens in less than 10 years".

We Europeans need to balance a strong regulatory environment with one that fosters innovation and competition so that youth and skill have a chance to overcome age and treachery. Basically, let’s do what Mario Draghi said.

Over-regulation will only hand the advantage back to better-resourced behemoths. So, if any EU payments regulators are reading this, please heed the words of a man with money as his namesake, one Johnny Cash, and "walk the line".

This is the only way we will reduce the barriers to entry for homegrown fintech challengers so that one day they too can become old, treacherous and unimaginably rich.