Why Germans love cash

In 1000 words.

The average German has €1,364 in cash at home or in a safe deposit box, and carries €107 in their wallet when they leave the house.

There are three broad theories to explain why Germans love cash and insist on using it in many situations where an electronic payment would be more convenient for the customer.

Theory #1 : the psychosocial imprint of authoritarianism in the 20th century

Within living memory Germans have lived through two types of authoritarianism : fascism (Third Reich + Gestapo) and communism (DDR + Stasi). Both regimes used personal data to track, arrest and murder dissidents. This makes many Germans highly sensitive about what personal information they share, including transaction data. Cash, on the other hand, is anonymous and difficult to trace.

Related, but subtly different, is the idea that holding cash gives an individual or business more control. If you keep it in a safe or under your mattress, you have access to it whenever you need it, independent of a bank or third party - and most importantly, these organisations cannot deny you access by freezing accounts or going offline. I am sympathetic to this last point, as many business owners who use the likes of PayPal have had their funds frozen over transaction disputes, tying up much needed working capital. I have written about this in more detail here.

Theory #2 : physical characteristics, truth and guilt

The Germans have a well known saying that “nur Bares ist Wahres” (Only cash is true). This implies that the physical characteristics of cash make it more reliable, honest and truthful than digital equivalents. Having lived here for 6 years and having worked in more digitally advanced economies like the UK and USA, my personal view is that Germans are not early adopters of new fangled digital technologies.

As former German Chancellor Angela Merkel gaffed at a press conference with Barack Obama as recently 2013; the internet is Neuland (“uncharted territory). Well, not really.

This digital illiteracy perpetuates, among other things, the belief that holding cash is better for budgeting because it allows you to know what you have spent and what you have saved.

Germans are also more averse to debt than almost any other nation on the planet, both as individuals and as a government, which is why the German government has an enforced debt brake and limits on borrowing as a percentage of GDP, resulting in one of the lowest debt-to-GDP ratios of any industrialised nation.

The aversion to debt is bound up with the German language, where the word Schuld means both 'debt' and 'guilt’. Tough.

In the context of payments, this looks coincidental. Payment upon invoice is still one of the most popular payment methods in German e-commerce and gives consumers the opportunity to assess the quality of the goods purchased before deciding to keep them, or return them. Perhaps because there are clear payment terms it is not perceived as “debt” per se by German consumers. But then isn't a credit card exactly the same? And Germans are not so keen on these?

Theory #3 : Efficiency and reliability

Cash is a highly efficient, cost-effective and reliable medium of exchange, and Germans love things that work. This is a nation built on engineering and manufacturing after all, although the idea that German prosperity has been made possible by Vorsprung durch Technik is becoming harder to defend with each passing year, as industrial-scale innovation - and economic growth - stagnate in Europe's largest economy.

Between clinging to practices that have worked in the past and adapting to new realities, there is a huge tension. I wish more German consumers, and existing business owners would internalise Friedrich Schiller’s maxim:

“Wer nicht mit der Zeit geht, geht mit der Zeit” (Those who don’t go with the times, will in time go)

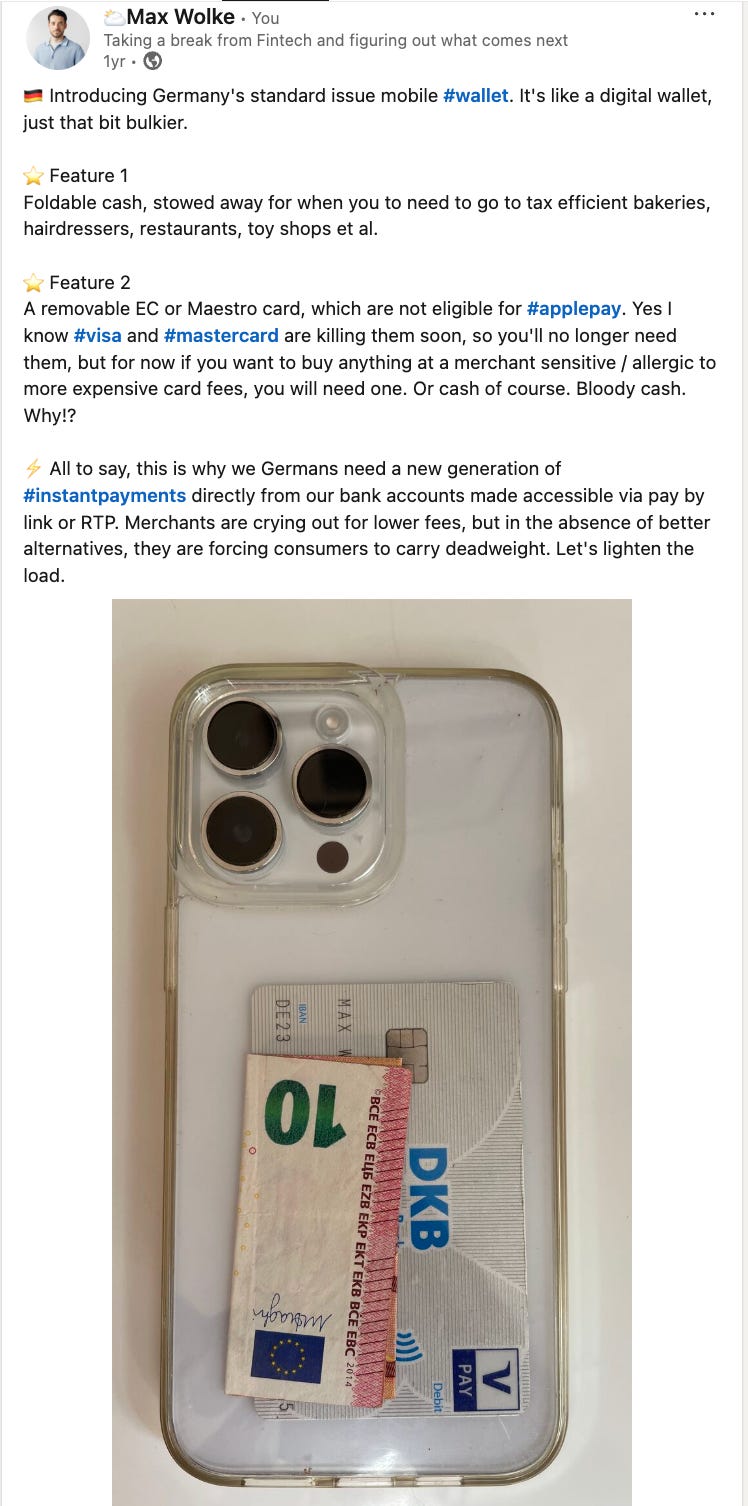

This is related to another German trait, which is a tendency to optimise for the bottom line, rather than thinking big and growing the topline. Restaurants, taxis, bakeries and many other small businesses have a visceral dislike of card and PayPal transaction fees, which range anywhere from 0.5% to 3% depending on volumes. Many see this a tax on their business, rather than a way of making payment more convenient for their customers. And in many instances, it costs them in lost sales as customers without cash walkaway and go somewhere else. (There are of course costs associated with cash management - something I have pointed out to many German business owners over the years, with limited success).

This means that many establishments will happily direct you to the nearest cash machine rather than accept an electronic payment. Data from the German Retail Institute (EHI) shows that a whopping 35.5% of retail payments (petrol stations, pharmacies, e-commerce et al.) are still made in cash, compared to nearly 0% in countries like Sweden. Fortunately, I have found that most taxi drivers will reluctantly take a card reader out of their glove compartment if you make enough of a fuss about being forced to pay in cash. Or accept a friends and family PayPal transfer.

That said, cash is very reliable and not subject to system outages, which means you can use it to buy a cold beer and a sausage in a mountain hut in any weather. That's not always the case with "temperamental" card readers.

All theories are necessarily simplifications of complex causes and effects.

I think Germans' relationship with cash is probably a mixture of all three theories and a few sub-branches of each. And depending on who you talk to, they will place different emphases on each, although data privacy in the age of surveillance capitalism is a constant concern for the majority of Germans.

Perhaps this is why a throwaway LinkedIn post of mine, written in haste before a lunchtime run, has generated so many emotive responses; 2 million views, 10,691 reactions and 674 comments to date.

I will continue to watch whether the Germans change their ways or stick to what they believe to be true. Being only half German, I can thankfully hedge my bets.

Hi Max, thank you for this post. I am thinking about this topic since many years and I would like to add a different view.

First of all I believe in the statement "convenience kills trust". This means for me, we would have seen a much higher adoption of electronic forms of payments if banks/financial service providers would have offered a better, more convenient way of paying. This also means, that from my point of view, theory #1 is weak. I know it is commonly used as an explanation but more as an excuse by banks to not deliver convenient solutions to consumers.

Banks didn't offer the right solutions (to consumers and merchants). PayPal, Apple Pay, and other US solutions had to come to Germany to provide the right solutions to consumers in Germany and... what a surprise consumer love it and use it massively.

So why didn't banks offer the right solutions to Germany? About 10 years ago, Germany had 10.000 contactless terminals, Netherlands none. 2 years later Germany had 30.000 and Netherlands hundred thousands. How come? A different market structure. Germany has a very fragmented banking market with > 1.000 banks, the Netherlands about 3 dominant players. Those 3 players, both issuer and acquirer, jointly started changing the market by issuing contactless cards and contactless terminals. This is how you drive and change an infrastructure.

In Germany, issuing is in the hands of thousands of banks and banks are (except cooperative banks and nowadays Deutsche Bank AG) no acquirers (anymore). This difference in the market structure is for me one of the most important factors why Germany in lagging behind when it comes to the use of electronic payments.

Look forward to further exchange on this - then hopefully in a personal meeting.

Christian